Recent Posts

Mentorship February 14, 2017

When you hear the phrase “retirement,” what comes to mind? Sandy beaches and afternoons of golf? Baking cookies with your grandkids? Hopefully the term “savings” also pops up – but if it doesn’t, you’re not alone. In fact, a 2016 survey found that 1 in 3 Americans don’t have a retirement plan.

READ MORE: 5 Ways Millennials Can Start an Epic Retirement Plan

One of the easiest ways to avoid becoming that “one” is to take full advantage of your 401(k) plan. To find out the 411 on 401(k)s, ENTITY reached out to Cameron Huddleston, Life + Money columnist for GoBankingRates, Andrew Eschtruth, associate director for external relations at Boston College’s Center for Retirement Research, and Katie Brewer, CFP®, Financial Coach to Gen X and Gen Y with Your Richest Life.

Here are five simple facts you need to know to get the most out of your 401(k).

First off, what the heck is a 401(k)!?! Basically, “a 401(k) is a tax-advantaged retirement savings plan offered by many employers,” explains Eschtruth. “Workers choose whether they want to participate in the plan, and then set aside a portion of their earnings [up to $18,000, or $24,000 for those age 50 and older] through payroll deduction. The employer typically provides some matching contribution as well.”

From 2009 to 2013, the number of companies who offer matching compensation dropped by 7 percent. So, if your company does participate in this program, use it – and research just how much your employer is willing to match. “The most common type of match is 50 cents to every $1 contributed by an employee up to a certain percentage of pay,” says Huddleston. “For example, if you earn $40,000 a year and contribute just 3 percent of your salary [a saving plan many employers set up automatically] but your employer offers a 50-cent match up to 6 percent of deferred salary, you’re missing out on $600 in free money.”

Some companies offer a 401(k) plan as soon as you sign on whereas others can make you wait up to one year. By knowing your timeline, you can start saving portions of your paycheck as soon as possible.

When you think of retirement savings, saving on taxes might not be the first benefit to pop into your mind. However, “because 401(k) contributions come out of your pay before taxes, your taxable income is reduced – essentially lowering the amount you pay to Uncle Sam and letting you hang onto more of your hard-earned cash,” according to Huddleston.

READ MORE: 5 Reasons Women Should Make Their Own Money

What can those savings look like? Turbo Tax gives this example: if you earn $35,000 a year and your tax bracket is 25 percent, contributing 6 percent of your salary – or $2,100 – into a 401(k) reduces your taxable income to $32,900. As a result, you pay $525 less in income taxes than you would for your full salary!

It is important to remember, though, that this money isn’t tax-free forever. You’ll have to give a portion to Uncle Sam when you eventually withdraw from your 401(k). As long as you wait until you’re retired to do this, though, you’ll be earning less money and will likely be in a lower tax bracket. This means you should pay less taxes on the money than you would’ve previously.

A 401(k) doesn’t just involve saving money, either. It also “provides some choice of investment options, typically in mutual funds,” according to Eschtruth. (Vocab lesson of the day: a mutual fund is a company that uses money from various investors – like you – to invest in securities like stocks, bonds and short-term debt).

READ MORE: Smart Investments Millennials Can Make to Prepare For the Future

Eschtruth points out that, when investing, you should pay attention to the costs of using different mutual funds. “Mutual funds that rely on following an index, rather than actively picking stocks, tend to have lower fees,” he says. “Overall, though, the best bet is to consider the potential rate of return a mutual fund offers [minus] the investment fees.”

Unless you’re a financial guru, investing probably sounds a bit scary. However, Huddleston says: “Don’t make it more complicated than it has to be. If your 401k plan offers a target-date fund or index fund, either can be a good place to start. A target-date fund adjusts your holdings of stocks and bonds automatically over time to reduce your risk as you near retirement age. An index fund tracks a major market index, such as the S&P 500, and typically has low fees.” Even better? Huddleston reports that many 401(k) programs come with investment advising services so you don’t need to figure all this out on your own.

If you’ve started building up your 401(k) but suddenly need to change employers, don’t panic. In this case, think of a 401(k) like the leftover data on your monthly phone bill: you can roll it over.

In fact, you typically have four options:

While it may be tempting to cash in that lump sum right away, that money comes with plenty of strings. If you don’t want to pay a 10 percent penalty tax, you need to wait until you’re 59 1/2 (or, in some cases, over 55) to cash your 401(k). This is why Eschtruth advises workers to “avoid taking money out of their 401(k) before retirement.”

READ MORE: Money Really Doesn’t Buy Happiness, According to Britain’s Youngest Lottery Winner

Basically? A 401(k) is an awesome tool to save up for retirement, even if you change employers…but it’s not a nest egg of hidden cash you can dip into any time you want to pay off debt or start a business.

Finally, one fact every woman should know: a 401(k) might even be more important for you than your husband or brother. As Eschtruth points out: “Women tend to live longer than men, so they should save sufficiently to build up a nest egg that can last them throughout their potentially longer retirement.” In fact, a 2015 report found that American women are living to 81.2 years versus men’s 76.4 .

Brewer also explains that women can end up saving less because they could “have seasons of their lives where they may be working part-time or taking time off from work. 401(k) contributions can only be made in the current year, so you can’t contribute more than the limit because you didn’t contribute the previous year.” So, if you’re working now, make that time count in terms of your 401(k) contributions.

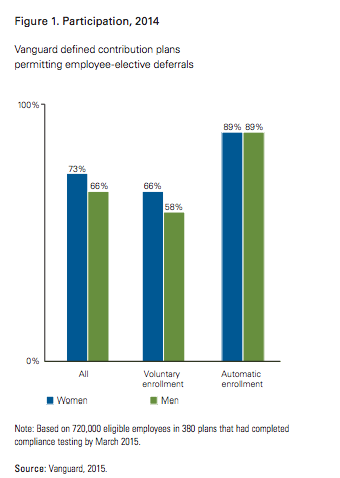

The good news is that women are 11 percent more likely to (voluntarily) take advantage of workplace savings plans, according to research from Vanguard. However, Vanguard also found that, because women earn less, women’s median account balances are 50 percent lower than men’s.

Huddleston’s advice? “Women should use an online retirement calculator to find out how much they need for retirement and to see whether they’re on track.” You’ve probably heard the saying, “Failing to plan is planning to fail.” When it comes to saving up for your retirement, this cliche is 100% relevant and true.

READ MORE: Women Are Having ‘Too Much Fun’ to Retire

All in all, you might have plenty of uncertainties about your long-term future, but your retirement funds shouldn’t be one of them. The 401(k) plan is designed to benefit, not hurt you – and, when used correctly, it can be exactly what you need to save up for the retirement of your dreams.